How to Calculate Fuel Cost Consumption for a Truck

Read Article

Subscribe to get useful tips and advice from industry experts looking to help solve your company’s cash flow needs delivered right in your inbox!

Managing cash flow is important. One way to bring down your business costs is to use a discount fuel card. Fuel cards offer significant advantages by providing discounts at the pump. Greater savings allows for increased investment in your business or even just more money in your pocket. Consider using…

As a trucking business owner, you need the right tools to keep your operations profitable. Two tools that boost your cash flow and savings are using a freight factoring company and a fuel discount card. The impact to your business becomes even more powerful when these two are combined. Learn…

Freight brokers provide access to loads and lanes that you may not otherwise be able to run, and those can become a fruitful source of revenue for your business. However, payments from freight brokers may be delayed, and despite your best efforts to vet brokers, you may find yourself in…

NOTE: This article is for education and reference purposes only. You should always consult a tax professional to discuss your specific situation and finances. It is nearly that time again – time to reflect on the year behind us, take inventory of our wins and losses, and plan for a…

Pierre Laguerre, Myles McGregor, Casey Cooper, Amari Ruff. These are just a few names of Black trucking business owners who built successful companies that have left lasting legacies within the industry. Within publications, podcasts and social platforms focused on Black business, transportation has become a hot topic the past few…

As a small fleet owner, a large portion of your operational spending goes to fuel, which must be planned for and controlled to maintain profitability and competitiveness. The Best Way to Plan for Fuel Expenses The first step toward efficient fuel expense budgeting is understanding the variables affecting fuel consumption.

For small fleet owners, or single-truck-owner-operators, the cost of doing business can be huge. Fortunately, there are ways for carriers to save on one of the most expensive business costs that can’t be avoided – trucking insurance. Insurance companies are looking for smarter and simpler ways for transportation companies to…

Dallas, TX, January 30, 2024 – Triumph, a member of the Triumph Financial, Inc. (Nasdaq: TFIN) portfolio of brands and a leading provider of working capital financing solutions to the transportation industry, announced today the appointment of Kim Fisk as EVP, Chief Operating Officer (“COO”) of its factoring division.

It’s no secret that you, as an owner-operator, can better manage your spending and save on fuel with the right fuel card program. But, what factors should you consider when making a decision? This is your road map for choosing the right diesel fuel card your trucking business. Whether you’re…

As a trucking business owner, you feel every dollar you spend, especially when it comes to fueling up. Diesel fuel is one of a trucker’s biggest expenses each month, but there are loads of discount fuel cards for truckers to help take away the pain at the pump. Before…

Triumph, a member of the Triumph Financial, Inc. (Nasdaq: TFIN) portfolio of brands and a leading provider of working capital financing solutions to the transportation industry, announced today the appointment of Jason Heilig to the position of chief technology officer of its factoring division. He will…

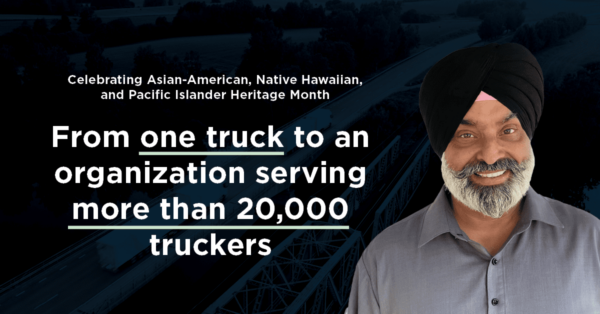

In celebration of Asian-American, Native Hawaiian, and Pacific Islander Heritage month, we’d like to highlight Raman Dhillon, founder of an organization helping more than 100,000 truckers – the North American Punjabi Trucking Association (NAPTA). Punjab is a region spanning Northwestern India and Eastern Pakistan that is…

With rising fuel prices, fuel fraud is on the rise, too. Here are some tips to help you make your account more secure and spot possible fraudster devices. Lower spending limits per transaction on your card(s) to what will be needed per fill-up. Limits can be set by dollar…

Triumph Business Capital, member of the Triumph Bancorp, Inc. group and provider of working capital financing solutions to the transportation industry, announced today its selection as a 2022 “Top Company for Women to Work For in Transportation” by Redefining the Road, the official magazine of Women In Trucking (WIT).

That’s a wrap! For the third time in four years, Triumph hosted its soccer tournament for more than a dozen transportation and logistics companies in the Chicago area on August 13. On a beautiful, 75-degree day, more than 300 fleet owners, drivers, family members, and friends made the trek to…

From the loading dock to the office, transportation and logistics companies are primarily made up of men. But, things are changing and quickly. Women in Trucking, an organization focused on gender diversity, non-partisan legislation, and job support, recently published a gender diversity index. According to the data, 39.6…

Triumph Business Capital (TBC) was highlighted in the July issue of SF Net’s “The Secured Lender Magazine,” an industry publication focused on the finance and alternative finance space. The most recent edition, which focused on ABLs and factoring companies, emphasized growth trends by product segment within secured and alternative financiers…

Fuel is one of the largest ongoing expenses for any fleet and is estimated to account for 24% of total operational costs. If fuel costs and usage are efficient, it would follow that the fleet itself is running efficiently as well. Unfortunately, managing fuel costs can be extremely challenging…

EDITOR’S NOTE: This blog is for educational purposes only. Please refer to the appropriate state and federal websites for more information. The trucking industry is dynamic, complex, and ever-evolving. Running a successful fleet or owner-operator business requires a deep understanding of various trucking regulations and new trucking laws. Staying on…

Building a successful and efficient fleet is no easy task. Tracking equipment, managing drivers, analyzing costs, ensuring regulatory compliance, and providing top-notch customer service are essential daily activities. But how do you know if you are moving in the right direction? Fleet management metrics and fleet utilization metrics provide the…

Truck drivers are often faced with long hours, hundreds of miles of highway, and a lot of time to tune into satellite radio or their favorite podcasts. With such a broad range of podcasts available, it can be hard to find high-quality content that is informative, relevant, and entertaining. Here…

Dallas – October 4, 2021 – Triumph Business Capital, a member of the Triumph Bancorp, Inc. (Nasdaq: TBK) group and provider of working capital financing solutions to small and medium-sized business, announced today the appointment of Rob Wright as chief product officer. Wright will report to chief executive officer, Geoff…

The second Chi-Town Showdown Soccer Tournament took place July 24 in Chicago, and FC Bodrost Chicago defended their title and took home another trophy. After a long day of tournament play, only two teams remained. FC Bodrost Chicago and Strong One Freight finished a close game with a final…

Dallas – April 26, 2021 – Triumph Business Capital, a member of the Triumph Bancorp, Inc. (Nasdaq: TBK) group and provider of working capital financing solutions to small and medium-sized business, announced today the appointment of Amber Roy as chief operating officer. Roy will report to its chief executive officer,…

The transportation world is always on the go, sometimes making it difficult for carriers who spend their days on the road to stay up to date with new developments. That’s why trucking events and expos are so valuable. As long as you can find a weekend to attend – in person or online — one of these transportation events…

There is a lot of excitement going around for freight broker events in 2021. These events will showcase new technology, introduce new industry-specific knowledge, and give you an idea of where the logistics space is headed. No matter what size broker you are, you’ll find an event that’s perfect for…

Being the owner and operator of your own trucking business is a huge opportunity for a lot of people. The ability to be your own boss, call all the shots, and build your business from the ground-up has enticed people for generations. If you’re thinking about getting…

Not knowing what you don’t know can put you out of business. On average, we see one factoring client per day shut their doors due to the inability to service ACH bank withdrawals associated with Merchant Cash Advance and other Cash Invoice Advance Loans. If something seems too good to…

The coronavirus has forced everyone to take a step back from trying to improve their cash flow and take a ‘get back to the basics’ approach. The ability to build a professional network and strengthen existing relationships or make new contacts is just one more area of business that has…

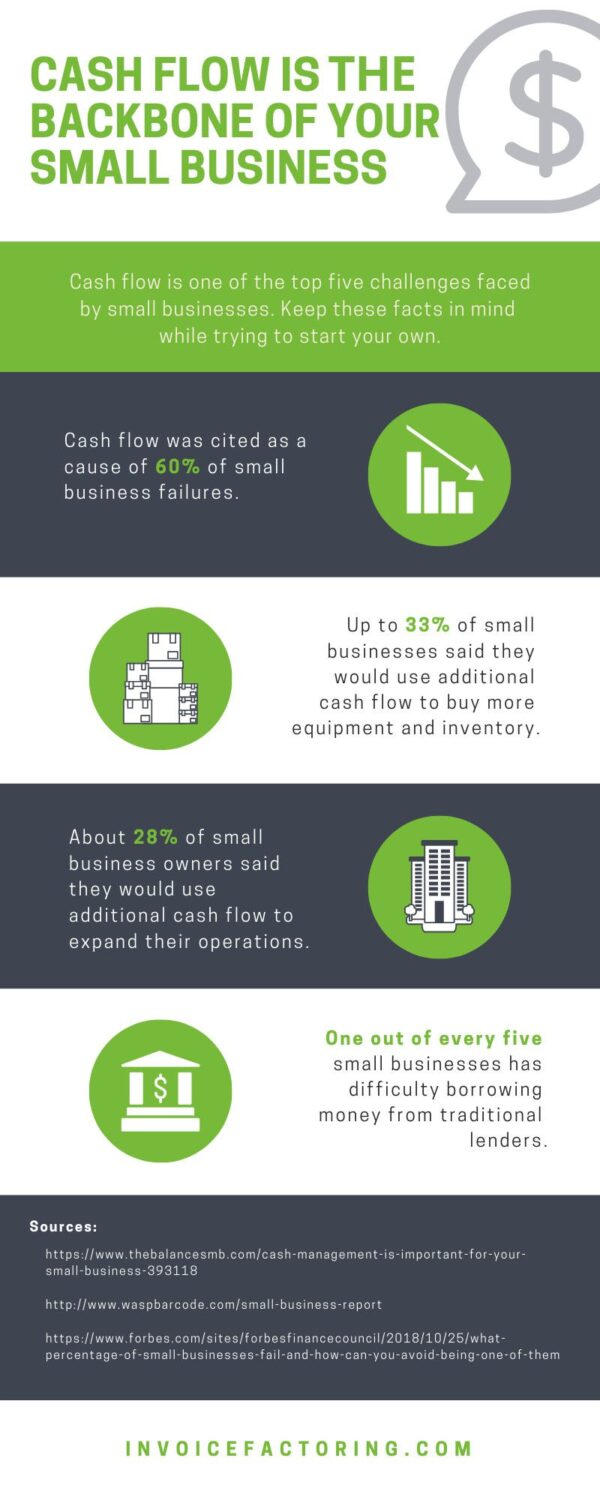

Working capital is the life blood of every small business. Without working capital, you won’t have the money to pay overhead expenses, purchase raw materials, meet your payroll, or pay your vendors. In fact, a lack of working capital combined with poor cash flow is behind most small…

DALLAS, TEXAS Triumph Business Capital, member of the Triumph Bancorp, Inc. group and provider of working capital financing solutions to small- and medium-sized businesses, announced today the hiring of Erik T. Bahr as executive vice president of sales. He will report to Geoff Brenner, chief executive officer.

The trucking industry is a unique one, but it is not exempt from the digital age that we are living in today. According to our invoice factoring company, while truckers of the past may not have seen a need for a website, there are a few reasons why you…

Many owner-operators start to consider factoring or take broker QuickPays when they don’t want to wait more than a few days to get paid on a delivered load. You can’t afford to turn down loads, but you can’t run your business without consistent income. This is why broker QuickPay and…

As a leading invoice factoring company that offers tailored solutions to the trucking industry, we know that fuel is one of your biggest expenses. Knowing how to calculate fuel cost consumption for a truck is essential for all trucking companies of all sizes, from owner-operators to fleet owners. Without knowing your…

The freight broker game continues to change the way that cargo is moved. Technology now dominates an industry that used to require nothing more than a telephone and a poster board. Staying on top of the changes in this fast-paced industry requires knowing what’s trending and what new tech is coming…

Trucking events can be some of the best ways for busy, on-the-road carriers to see what’s going on in the world of transportation. Many shows have huge expo halls that you can walk and get a glimpse of the latest and greatest products on the market for truckers. …

As a factoring company, we talk to business owners everyday about cash flow. Some complain about slow payments. Others work in unpredictable or seasonable industries and are looking for some help to make it through the harder months. In either case, the…

Is next year the right time to pursue your dreams and start your own trucking business? It could be. With an estimated shortage of 60,000 truckers nationwide (with estimates it will hit six figures by 2024), there will be plenty of opportunity to become an owner-operator…

It doesn’t matter if you just started your business, or you’ve been around for years. There are basic terms and definitions that every entrepreneur should know. Not knowing the basic definitions of common invoice payment terms can cause confusion between you and your client, set the…

Accounts receivable financing is one way business owners speed up payment on B2B invoices. Many or most invoices are Net 30, (meaning the customer has 30 days to pay). Some may even extend out to 90 days or more. Waiting this long for…

If your business is running short on working capital, it can totally derail operations and add to your stress. The good news is there are lots of ways to remedy this all-too-common situation. Many business owners assume that a loan or credit line alone…

It’s no secret that demand for trucks has been down compared to 2018. If you follow trucker message boards or social media groups, you’ll find a lot of truckers wondering where all the loads went. To put it more bluntly, they’re wondering where all the high-paying loads went. …

Technology drives the transportation and logistics industry. This isn’t news to truckers. Smart phones have changed how freight gets moved. Trucks are now integrated mobile offices. By using apps and other mobile technology, transportation companies want to streamline the entire load delivery process. Depending on…

Every industry has its challenges, but the oil and gas industry is arguably one of the most difficult for a variety of reasons. Like any business, oil and gas companies face a mix of financial and operational roadblocks that can hurt production. More than that, oil and gas companies are…

Starting a business requires a leap of faith. Even when you know you’ve got the skills and know-how to be a success, there are many ways that your budding venture can go wrong. Arguably, the toughest part for any entrepreneur is securing the funds to gain traction and grow despite…

Every business has rough patches — times when money is tight, and you’re wondering how you’ll make ends meet. As of 2019, more than half of all start-up businesses will fail within four years. A lack of money is the no. 2 reason that businesses fail. A lack of…

If you’re new to invoice factoring, you might come across some terminology that you’ve never seen or heard before, it can be a little bit like learning a new language. At Triumph Business Capital, we always want our clients (and potential clients) to understand what we’re…

Every small business owner knows that cash flow is the life blood of a company. With it, you can purchase raw materials and inventory, pay your overhead expenses and keep up with payroll. Without it, you may find yourself unable to fill orders or meet your financial commitments. For these…

Small businesses are the life’s blood of the US economy. According to the SBA, there are 30.2 million small businesses in the United States as of the end of 2018. Every business has its own challenges and goals in 2019. We’re already at the end of 2nd quarter, and you may have…

As a small business owner, you know that staying on top of cash flow can be a challenge. Without adequate cash flow, you may be unable to meet your financial obligations and, as a result, your growth can stall. As we’ve discussed in previous blog posts, partnering with an invoice…

You’ve launched a business, built a team, and attracted a base of clients who love what you do. In other words, you’ve become a real-deal entrepreneur. So now what? If you want your company to continue to grow, you’ll need to finance your business for both the short term and…

There are more than 30 million small businesses in the United States, and no two are exactly the same. However, there are some problems that are common to many small businesses and one of those is money management. If you have issues with cash flow or financial management, it can negatively…

Starting your own small business requires dedication, planning and resources. You might be committed to starting your own company. You have a business idea, and you can’t wait to act on it. But what do you need to start a small business and turn it into a success? How do…

There are many financial issues freight company owners must manage on a regular basis. The rising costs of trucks and equipment are in direct conflict with long waits for shipping payments, and it’s a combination that can create gaps in cash flow. Cash flow issues are one of the most common…

Small business owners sometimes struggle with managing cash flow and finding the working capital to grow their companies. Invoice factoring is a form of accounts receivable financing that provides you with a cash advance on your invoices that are due within the next 90 days. Is factoring right for your…

Consistent and predictable business cash flow is a must if you want your business to grow and succeed. In fact, 82% of all business failures are linked to poor cash flow management. That’s a statistic you can’t afford to ignore. Fortunately, there are some practical steps you can take to even out your…

The majority of small businesses fail within the first five years. Cash flow was cited as one of the main causes among 60% of failed small businesses. Although every business has its financial peaks and valleys, small businesses are especially susceptible to gaps in cash flow because of their limited…

Every business wants to increase its profits, but those profits are especially crucial to small businesses. Even the smallest reduction in expenses or increase in revenue can have a major impact on your profitability. The good news is you don’t need to completely overhaul your company to start seeing…

It can be stressful and frustrating when your business experiences cash flow fluctuations. These fluctuations are often the result of payment gaps in your accounts receivable. Simply put: you’re not getting your funds fast enough after completing your service or projects. This is where business factoring comes in. Factoring services…

We’ve discussed the benefits of invoice factoring in previous blog posts. From improving cash flow to providing stability, small businesses of all types and sizes — even trucking companies, — use and benefit from factoring companies to help their enterprises grow. Factoring companies specialize in helping small businesses drastically…

As we’ve discussed in previous blog posts, invoice factoring is a type of accounts receivable financing that converts outstanding invoices — due within 90 days — into immediate cash for your business. But before you sign any type of contract or agreement for an invoice advance loan, it’s essential…

Cash is essential to any business, and there’s a debt-free commercial finance option that ensures that you receive it quickly. It’s a dependable, low-risk alternative when compared to a line of credit or a loan, and you certainly won’t have to spend weeks applying for it. We’re talking about…

What is invoice factoring? Invoice factoring can be particularly useful for small businesses looking to keep their cash flow moving and their resources consistent. Invoice factoring helps B2B companies boost their cash flow based on their outstanding invoices. This means immediate access to your money without having to wait for…

Working with commercial invoice factoring companies has numerous benefits and can provide near immediate cash flow for your business. In fact, factoring companies can help small businesses bridge invoice payment gaps with upfront payments, providing nearly all of the original invoice amount. That money is then immediately available for…

Economies are unpredictable and demand for certain products or services ebbs and flows depending on any number of reasons. Bankruptcies in the U.S. increased to 25,227 companies in the second quarter of 2016 alone. It’s important to stay on top of corporate finances, especially in the early stages of business…

It may sound shocking, but it’s true: Nearly 60 percent of invoices are paid late. Considering the fact that small businesses (defined as businesses with fewer than 500 employees) account for 99.7 percent of all business in the United States, late invoices are often a sign of a bigger financial…

Small businesses (defined as businesses with fewer than 500 employees) account for 99.7 percent of all business in the United States, making them a fundamental part of the economy. But anyone who’s ever owned a small business can tell you that it’s not always easy to stay afloat when it…

According to the Federal Motor Carrier Safety Administration, approximately 5.9 million commercial motor vehicle drivers operate in the United States, and many of them frequently take advantage of load boards as well as load factoring companies, also known as invoice factoring or freight bill factoring companies. Factoring companies can…

Your business credit score is something that can have a huge impact on how you’re perceived by your customers, competitors, and potential lenders and investors. The higher your score is, the more credible and trustworthy you’ll seem. Invoice factoring is a form of business financing that can impact your…

Invoice factoring is a type of accounts receivable financing that converts outstanding invoices due within 30, 60, or 90 days into immediate cash for your small business. While invoice funding companies work with businesses in many industry sectors, staffing agencies are looking to invoice factoring services for help with…

MARCH 5-8, 2019 The Work Truck Show, Green Truck Summit, and Fleet Technical CongressIndianapolis, IN The must-attend event for the work truck industry. North America’s largest work truck event is your once-a-year chance to see all of the newest industry products. More info: worktruckshow.com MARCH 10-13, 2019 TCA (Truckload Carriers…

Nearly 12 million trucks, rail cars, locomotives, and vessels move goods over the transportation network. Commercial transportation requires a great amount of attention to detail, which is just one reason so many professionals have been relying on services from transportation factoring companies and other types of small business factoring.

Nearly 12 million trucks, rail cars, locomotives, and vessels move goods over the transportation network. Every load has a lot of paperwork – rate confirmations, BOLs, lumpers, detention. You get it. It’s a lot of paper for one load. So how can owner-operators manage all that paperwork, submit your invoices…

MARCH 5-8, 2019 The Work Truck Show, Green Truck Summit, and Fleet Technical Congress Indianapolis, IN The must-attend event for the work truck industry. North America’s largest work truck event is your once-a-year chance to see all of the newest industry products. More info: worktruckshow.com MARCH 10-13, 2019 TCA…

As a trucking owner-operator, you know that running a successful business requires you to wear many hats. You’ve got to be thinking about everything from gas mileage to depreciation to cash flow. The new year is here, and that means this is a good time to look to the year…

Is cash flow an issue for your trucking business? If so, you should consider freight bill factoring. You need funds to pay expenses and grow your business, and you can’t always afford to wait 30, 60, or even 90 days for customers to pay. Fortunately, invoice factoring can help bridge…

Owning and managing a freight company isn’t easy. In the course of the day, you may wear many different hats: owner, manager, accountant, marketer, and human resources manager, to name a few. And when you’re juggling so many things, it’s easy to let something important slip through the cracks. That’s…

The holiday season is here, bringing days of celebration and fun. But, for many small business owners in the United States, it also brings some anxiety. How will they keep up with increased holiday orders, pay for inventory, and keep their businesses afloat? According to the Small Business Administration,…

It’s been estimated that if all invoices were paid on time, U.S. small businesses could collectively hire 2.1 million more employees, which would reduce unemployment by 27 percent. That’s just one reason why more and more businesses are working with invoice and freight bill factoring services. But before you…

Invoice factoring is a type of accounts receivable financing that converts outstanding invoices into immediate cash for your small business. There are many different types of invoice factoring, from small business factoring to trucking factoring services. Before you determine whether or not your business could benefit from factoring, it’s…

We’ve discussed in recent posts how invoice factoring works: it’s a type of accounts receivable financing solution that converts outstanding invoices due within 90 days into immediate cash for your small business. And while many business owners assume that they need good credit to qualify for funding for their…

Invoice factoring is a type of accounts receivable financing that can help small businesses avoid wait times of up to 90-plus days for customer payments. And while it’s ideal for countless types of small businesses across many industry sectors, it’s particularly popular for freight and trucking companies. Nearly 12 million…

Invoice factoring can go by many names: invoice financing, invoice funding and accounts receivable financing. Different names, but they all help small businesses receive the funds they need without waiting 30, 60 or 90 days to get paid from their customer. In many cases, invoice factoring services can provide funding…

Making it as a small business isn’t easy, no matter your industry. Rarely, can small businesses survive waiting 30+ days for payment, especially when their vendors are calling for their payment. If you find yourself struggling to manage payroll, rent and other overhead costs while waiting for payment, you have…

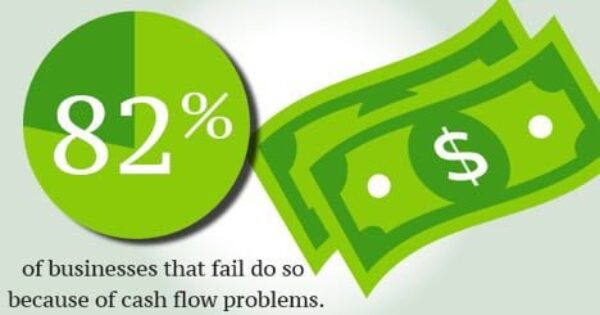

There are nearly 28 million small businesses in the U.S., and in today’s uncertain economic climate, many small businesses struggle to stay afloat as a result of insufficient funds. In fact, according to a U.S. Bank study, 82 percent of businesses that fail do so because of cash flow problems.

When you’re on the road, you need to make sure you can afford to maintain your truck as well as your business. Cash flow is critical to truckers and trucking companies, which is why we have a solution —freight factoring services. What exactly is freight factoring? Freight invoice factoring allows…

The start of a new year is a great time to take stock of what you want to achieve and what it will take to reach your goals. We wish you great success as an owner-operator in 2020, and offer some practical do’s and don’ts as you rev up for…

Invoice factoring has been around for thousands of years and can be traced to the 18th century B.C. Babylonian king, Hammurabi. Over the past 10 years, transportation intermediaries are directing more and more of their carrier payments to factoring companies ‐ anecdotally, we hear as much as 80%.

Freight brokers pay carriers – that’s what you do. You do it for fuel advances and again when the load’s settled and billed. You pay when it’s due and sometimes you pay quick. You pay by fuel card, by express check, by bank draft, by paper check. And mostly…

Cash is king. You know this as well as anyone else. Without cash, you can find yourself in some pretty uncomfortable situations, like not having enough money for payroll, or making late payments to vendors and bill collectors. So what can you do to manage…

It’s not only been days, but weeks—or even months—since you performed work for your client, and you still haven’t received payment. Sound familiar? As a professional, you need to be paid on time. You’ve got people to support and bills to pay. You may be considering…

Let’s face it, money can get in the way of any relationship, whether business or personal. And small or mid-size business owners like you never want to compromise relationships with customers or vendors. But without the funds to pay your bills on time…

You’re running a small or mid-size business and that takes money—lots of it. But coming up with the capital you need, when you need it, can often pose significant challenges—like how to meet payroll, pay vendors, upgrade equipment . . . the list goes on and on. So…

Don’t you love that feeling—you know, the one you get when an invoice pays? With invoice factoring, you don’t even have to think about processing invoices, and you can forget about having to wait 30, 60, or 90 days to receive your client’s payment. You can actually…

Invoice factoring and a bank loan have very little in common—other than the fact that both provide cash to finance small businesses. Here’s a simple factoring vs. bank loan comparison to help you decide which can work for your business. Invoice factoring With…

What are some of the popular types of short-term funding available to small businesses? How can you fund your business? You’ve got questions; we’ve got answers! 1. Bootstrapping Bootstrapping is a funny word for a smart financial concept. The term comes from the phrase “pulling oneself…

It’s a big world out there. We’re talking the world of funding for small- to medium-sized businesses. That’s why we’re giving you a bird’s-eye view of the available options—everything you need to know about funding your business. Invoice Factoring You may have heard of…

Invoice factoring is a saving grace for many industries, from transportation and staffing to small and mid-size businesses as well as government contractors. In fact, invoice factoring can offer welcome financial relief if you’re just starting a business, have bad credit, can’t get funding from banks, or are at…

Many businesses turn to Triumph Business Capital to get their invoices factored for relief from today’s financial pressures. Faster and easier than a bank loan, getting an invoice factored doesn’t rely on your credit or your years in operation. You simply convert your invoices into immediate…

It’s a headache and a hassle, and it causes complete confusion—It’s the Net-30 Trap. Does it mean you get paid 30 days from the date on the invoice, 30 days after the client bills their client, or within 30 days of what exactly? Do you get paid at all? What…

You do the work, deliver the product or service, and wait. And wait. And wonder—will you get paid on time or have to make countless calls to get your money? Let’s face it. One of the biggest challenges facing small and mid-size businesses (SMB) is getting paid—especially since many companies…

On May 5, 2016, many schedule contractors received a notice of the government’s continual examination of compliance to the Trade Agreements Act (TAA). Schedule contractors are required to remain TAA compliant with this act by verifying the country of origin for all of their products. If you are…

You took the leap and started a business, but now you lie awake at night feeling like a fraud, like you don’t deserve the success you’ve created. It’s called imposter syndrome, a term coined in 1978 by two clinical psychologists referring to high-achieving individuals who are unable to internalize their…

1.9 million college students are expected to graduate this year and most of them will want to start their career right after they walk across the stage. By targeting college graduates, your staffing agency can dip into a talent pool that comes to the workforce with fresh, new ideas and…

Freight brokers have a lot of responsibilities, from matching shippers and carriers to making sure each piece of cargo gets to the right place. Another essential task in this busy industry is bookkeeping. Freight brokers who don’t prioritize bookkeeping can end up losing money in the long run. Here…

After the first lesson in this series, you now have your social sites all set up and are ready to engage your followers. People want go where content is fresh, new and relevant. No one likes or follows a page with stale content. With an abundance of ideas on what…

In 2009, a trucker named Jason Rivenburg was shot and killed by a man who stole $7 in cash from him. Forced to park in an abandoned gas station when he became tired, Jason became the victim of a brutal crime. Sadly there are other stories similar to this one;…

If you work for a staffing agency, social media can be a powerful tool to help your firm grow by finding the right candidates. Agencies that aren’t utilizing social media marketing in their strategy are missing valuable opportunities. However, with many platforms available, it can be challenging to determine which…

Whether you realize it or not, at some point in your career you will inevitably face the need to sell something, be it a product or service, or even yourself as a qualified candidate in a job interview. Learning how to effectively close the sale, regardless of what’s at stake,…

When small businesses have a need for money, the most common next-step is to apply for a loan. What many don’t realize is that they have capital readily available to them in the form of outstanding invoices. In fact, the process of accounts receivable factoring has many favorable benefits over…

When you search for freight broker training courses on Google, you will inevitably find pages and pages of results. How can you decipher which one is best for your freight brokerage? More importantly, how can you determine which freight broker training course will provide the best return…

According to the Centers for Disease Control and Prevention, a trucker’s life expectancy is 16 years shorter than a normal life expectancy. That outlook seems bleak for many, so the transportation industry has shifted its focus. With multiple resources now available for health and overall wellness, truckers can overcome the…

Purchasing a truck can be a significant expense, even for the most established trucking companies. As with most vehicles, acquiring a truck typically requires either a lease or a purchase. Which is the wisest investment? Let’s take a look at some of the pros and cons associated with each option…

You’ve probably heard the well-worn story of Goldilocks and the Three Bears. In this age-old tale, young Goldilocks is out for a walk in the woods when she stumbles upon the cabin belonging to the three bears. Upon entering and realizing nobody was home, she tests out each of the…

Keeping up with the demands of a successful business venture, while at the same time, trying to achieve ongoing growth can be quite challenging – even for the most seasoned professional. Whether it’s expanding to reach new market segments, opening additional locations, hiring more employees or whatever else the case…

The freight brokerage industry is one of intense competition. While being flexible is important, identifying a specific niche to focus on can help your firm stand out and improve your chances of sustained profitability. Some freight brokers naturally know what markets they should target based on their experience within…

Cash flow problems can cause you to put the brakes on your trucking business. Before you find yourself running on empty, take a look at freight factoring; it’s cash flow without debt. You may have heard of this type of financing before around the truck stop or at trade…

Social media is revolutionizing our world, not only in the way we connect with others but also how businesses market. With 74% of internet users using social media, small businesses can’t ignore that a large part of their audience are active on social networking sites. This audience is filled with…

Utilizing software product can play a big role in the success of a freight brokerage for a number of reasons. First, it can help streamline operations. It can also dramatically improve efficiency and productivity levels. Finally, it’s one of the most effective ways to maintain compliance at all times.

Driving a truck may seem pretty simple and straightforward, but given the size and power of these vehicles, safety is critical. That’s why a significant portion of all truck driver training programs is devoted to teaching future drivers how to keep themselves and other operators safe on the road, while…

Did you know that the U.S. government actually has a goal to award nearly one-quarter of its prime contracts to small businesses? Furthermore, Congress approves over $1 trillion in spending just about every year. Though this is great news, a good number of small businesses are still hesitant to get…

It’s that time of year again – tax season. As a small business owner, there are a number of unique considerations that you must account for while preparing to file. To make things a little easier, we’ve pulled together some best practices and small business tax preparation tips below. First…

Staying up-to-date on the latest recruiting strategies can be tough, particularly when it comes to attracting quality candidates from the millennial generation. The reason it’s so challenging is because individuals from this demographic are markedly different from previous generations. Before you find yourself frustrated and ready to throw in the…

With the new year comes concerns about staffing news and about correctly filing staffing taxes for your temporary staffing agency. Tax surprises are rarely good. Whether you have filed before or your agency is new within the last year, getting through tax season with accurate and acceptable payroll and tax…

The clock has started ticking. On December 16, 2015, the Federal Motor Carrier Safety Administration (FMCSA) published the official Electronic Logging Device (ELD) mandate, enforcing the adoption of ELDs by all truck drivers before December 18, 2017. Not only did the FMSCA publish this rule by Congressional mandate, but they…

4x BBQ World Champion, Myron Mixon, Explains How to use Triumph’s Web Portal and Mobile App in Less Than 10 Seconds. https://youtube.com/watch?v=j_AGPyuSdFQ My Triumph Web Portal and Mobile App With MyTriumph, you’ll see the real-time status of invoices purchased, which invoices are still being processed, and which items require your…

4x BBQ World Champion, Myron Mixon, Addresses Some of the Pitfalls of Truck Insurance. https://youtube.com/watch?v=j_AGPyuSdFQ https://youtube.com/watch?v=j_AGPyuSdFQ Triumph Truck Insurance Insurance is one of the major costs in any business operation. Sometimes, the type of coverage and payment structure can be the difference between success and failure of an operation. Triumph…

4x BBQ World Champion, Myron Mixon, Explains Triumph’s Online Broker Credit in Less Than 10 Seconds. https://youtube.com/watch?v=j_AGPyuSdFQ Online Broker Credit Our trucking clients can access freight broker credit checks through our online portal. We provide daily monitoring of over 80,000 freight broker and freight forwarder authorities. And free credit checks…

4x BBQ World Champion, Myron Mixon, Explains Invoice Factoring in Less Than 10 Seconds. https://youtube.com/watch?v=j_AGPyuSdFQ Invoice Factoring Deliver a load, submit your paperwork, and Triumph will pay your invoices in 24 hours or less. That’s just where we start. Triumph’s other services – online credit checks, fuel discounts, fuel advances, DAT load…

4x BBQ World Champion, Myron Mixon, Outlines the Government’s Hours of Service Regulations in Less Than 10 Seconds. https://youtube.com/watch?v=j_AGPyuSdFQ Hours of Service Regulations A rested truck driver is a safe truck driver. We agree. It’s not a hard concept to grasp – unless, of course, you are dealing with government…

4x BBQ World Champion, Myron Mixon, Explains Triumph’s Fuel Advance Program in Less Than 10 Seconds. https://youtube.com/watch?v=j_AGPyuSdFQ Fuel Advances Find a load and factor it through Triumph Business Capital, by sending us a request along with rate confirmation and bill of lading. In most cases, you’ll be eligible for a…

4x BBQ World Champion, Myron Mixon, explains which region of the country produces the best BBQ and why. https://youtube.com/watch?v=j_AGPyuSdFQ The Best BBQ in the country is…. Good food is good food is good food. The art, effort, and entertainment that surrounds preparing good food makes it special. As Myron says,…

4x BBQ World Champion, Myron Mixon, Explains Ascend2Triumph in Less Than 10 Seconds. https://youtube.com/watch?v=j_AGPyuSdFQ Just complete your load in AscendTMS, click “Get Paid”, and you’re done. The Ascend2Triumph seamless integration bundles up your completed load and invoice documentation with the click of a single button. No paper, no sweat, no…

It’s almost that time of year again – tax season. For truck drivers, there are many unique deductions available that can help reduce monies owed and maximize returns. Before sitting down with your accountant or tax advisor, here are some of the things to take into consideration that will help…

As a successful staffing professional, you’re probably in the process of setting your goals and objectives for the coming year. In doing so, it’s important to consider the trends that are expected to occur over the next 12 months. This will help you to better align your own business strategies…

As a small business, you face many challenges, particularly when it comes to competing with larger organizations. One area where this can be especially impactful is in the area of staffing. Simply put, it can be difficult to attract and recruit top talent when compared with some of the big…

Winning a government contract involves a lot more than simply drafting up a great proposal. It’s the relationships that you develop with the right people along the way that will ultimately bring you the success you’re after. To get you pointed in the right direction, here are a few…

The most important freight broker software system that anyone in the freight brokerage industry needs is a Transportation Management System (or TMS for short). A quality TMS can help you match the right carriers with the appropriate loads, route those loads most effectively and streamline other critical organizational needs…

Sandra Walls is President and CEO of AIL Logistics Solutions, a multimillion-dollar, Memphis-based, service-disabled veteran-, woman- and minority-owned company that provides diverse logistics and technical support solutions to government and commercial clients. A retired Lieutenant Colonel in the United States Air Force, Ms. Walls joined the company after serving 22…

Ask any CEO what the main challenges of their business are and in the top five will likely be attracting and retaining top talent for their business. Being able to provide your clients’ access to top talent in their industry can set your staffing agency apart from others. Even if…

The freight broker life can be a stressful life. You spend your days as a middle man working with shippers and carriers to get loads from point A to point B. Stress really sets in when it’s time for your carriers to be paid, but the shipper hasn’t paid…

When they’re done right, phone interviews can save time by pre-screening candidates and provide information you won’t find in any resume. Done poorly, they can be awkward, impersonal, and ultimately ineffective as a screening tool. These 10 Tips will help you become a more effective interviewer, and narrow down candidates…

Sandra Walls is President and CEO of AIL Logistics Solutions, a multimillion-dollar, Memphis-based, service-disabled veteran-, woman- and minority-owned company that provides diverse logistics and technical support solutions to government and commercial clients. A retired Lieutenant Colonel in the United States Air Force, Ms. Walls joined the company after serving 22…

Even in the age of social media, there’s no substitute for real relationships. With today’s online load boards, social media networks, and nationwide WiFi, it’s possible for a freight broker to schedule a load without ever coming face-to-face with the carrier. You might not even have to pick up…

The weather outside is frightful, but these winter trucking tips should make your drive a little more delightful. First, preparing for your drive starts before you even get on the road with a pre-trip inspection. You should already be completing a pre-trip inspection, but with winter road conditions, it’s recommended…

I love a classic Christmas movie, and one of my favorites is How the Grinch Stole Christmas. The Grinch lives high on a mountaintop away from all the villagers of Who-ville. To ruin their Christmas, he decides to sneak into town while they are all celebrating Christmas to steal all…

MC numbers. MX numbers. FF numbers. Soon, they’ll all be gone. In the near future, all interstate motor carriers will need just one number to complete the Federal Motor Carrier Safety Administration’s (FMCSA) registration process. Read on to find out why the change is happening, who is affected, how to…

What’s worth more — your money or your time? If you’re considering filing a patent on your newest invention, you could be spending a lot of both. However, conducting a thorough patent search as early as possible could save you time and money in the long run. We recommend contacting…

Last year, the U.S. government shelled out $447.6 billion in contract spending. Want a piece of that action? Becoming a government contractor definitely has its benefits, but if you’re thinking about taking the plunge into performing government work, it’s important to weigh the pros and cons first.

Good pay. Control over your hours and benefits. Less time behind the wheel — and more time with your family. There are many reasons to become a freight broker, especially if you have a history of working in the trucking industry. According to payscale.com, freight broker…

If someone were to ask me what app I use most on my phone, it would have to be my banking app. I am constantly checking my account. Some might find this obsessive, but I was a victim of a data breach a year or so ago, and I am…

Part 2 of an interview with Stanton Williams, a growth-driving president/CEO with two decades in the financial services industry and co-founder of a mobile app/social media technology venture. In this article, he discusses the role of a company’s chief operating officer and the importance of identifying the right person for…

Stanton Williams is a growth-focused president/CEO with extensive experience driving results in a fun, accountable culture. He recently acquired and became CEO of V-Rooms, a 10-year-old company that enables the secure sharing of sensitive business documents. Prior to that, he was a cofounding partner of Reach 1-2-1 Mobile, a mobile…

High pay. Growing demand. Stable industry. It’s a good time to be a freight broker. Here’s what the industry looks like today. If you’re considering becoming a freight broker — or wondering if you’ve made the right choice — we’ve got good news for you. Despite recent setbacks, the…

The average life expectancy in the U.S. is 78.7 years — but for truckers, it’s only around 60. While job risks like traffic accidents are partly to blame, the trucking lifestyle may be the bigger culprit. Here’s what truckers are doing to change the statistics, and create longer, healthier lives.

Economists say post-recession growth is sluggish — but the staffing industry is doing great. Read on to learn how staffing growth compares to the overall economy, which sectors are growing fastest, and what to expect in 2016. Long Recession. Slow Recovery. Unemployment is down. Job growth is up. So, why…

Thousands of rules and regulations. Hundreds of line items and questions. One blank sheet of paper. If you’re dreading the process of writing a government proposal, read on. These quick tips will help you get started writing the best government proposal possible — and they maybe even help you…

Hunter S. Thomson wrote, “Anything that gets your blood racing is probably worth doing.” What he did not specify is HOW to get your blood racing. If you know Mr. Thomson and his work (“Fear and Loathing in Las Vegas,” among others) you know he probably meant something illegal! However…

Thanks to the U.S. Small Business Administration’s 8(a) Business Development Program, economically and socially disadvantaged business owners can land new opportunities to participate in America’s mainstream economic engine. Success in obtaining 8(a) certification can propel the growth of eligible small businesses through lucrative opportunities in the federal marketplace. 8a eligibility…

Before new customers arrive at your front counter to check out, there’s a high probability they will first turn to their mobile devices and do a local search. Out of every three customers, at least one of them performs local searches prior to shopping. Google statistics show a compelling 73…

So you’ve decided to leap from employed trucker to becoming an owner-operator. There are definite advantages to having your own authority and being your own boss: setting your own schedule; choosing loads and lanes that suit you; leaving company politics, rules and dispatcher favoritism in your rearview mirror. But where…

As a staffing agency recruiter, you’ve been rewarded with revenue and loyalty from great hires – and felt the fallout from bad ones. According to the Harvard Business Review, bad hiring choices result in 80 percent of employee turnover. No wonder companies today are being more cautious. And, it makes…

Freight brokers and other transportation intermediaries, commonly known as third-party logistics companies (3PLs), play a key role in domestic and international commerce. You may not be aware that there’s an organization specifically dedicated to advancing your interests by marshaling that collective power: the Transportation Intermediaries…

What could you do with $1,080 extra per year, per truck in your fleet? You could be saving this much or more just by using the right discount fuel card. With so many fuel card options available, it can be hard to know how to choose…

You can probably recite a slew of metrics about your own operations, but you may not be aware of the role trucking plays in the U.S. economy or the extent of its reach. Here are 15 interesting tidbits about the industry you live and breathe: Charles Freuhauf invented the first…

Even though a freight broker is entrusting your trucks and drivers with their customers’ shipments, you’re on the hook if they’re not trustworthy, financially strong or a performance-focused owner-operator. Here are the top six questions to ask before you take on a job with a new freight brokerage. Is…

Making sure that employees’ paychecks are correct and on time – every time – goes a long way in keeping them satisfied. If your staffing agency fails to pay employees correctly, watch out for poor performance and low morale. And that’s just the beginning. At least 33 percent of businesses…

As a staffing agency recruiter, you understand the fallout that can result from an inadequate reference check when vetting job candidates. Not taking the time to do a thorough reference check, or asking the wrong questions can cost your firm in lost business, contracts and goodwill. In fact, a 2013…

The good news halfway through 2015: Unemployment is relatively low and staffing needs remain robust. But competition for top talent – individuals with coveted skills and capabilities – has ramped up too. This requires employers and staffing firms alike to bring their “A” game; maintain an appealing, dynamic presence using…

There are about 17,000 staffing and recruiting companies in the U.S., according to the American Staffing Association (ASA) — but not all of those agencies will succeed. The ASA recently reported that staffing industry growth is outpacing overall economic and employment growth,…

I’m an accidental entrepreneur. Thirty years I was a project manager in the marketing department of a North American specialty retailer, managing the production and distribution of signage and seasonal displays, and writing and overseeing merchandising guides, direct mail pieces, special event and other promotional materials for our 700-plus stores.

In my first year as a business owner, I made the same salary as when I was working for someone else. The second year, I doubled it. Once you get past the leap of believing you can make it on your own, the next big hurdle — having too much…

When I was building my business, I volunteered as programs chair on the board of a women’s technology nonprofit organization. I used my connections to help plan the first six months of programs for the following year and also coordinated logistics such as booking the restaurants for our meetings. I…

If you have $41,000 to spend on marketing, you can stop reading this article. That’s the average salary for a Social Media Specialist, according to payscale.com — and while it may not sound like much, it’s a lot for most small business owners. Fortunately, there are a number of free…

Want to learn all the rules & regulations of government contracting? How much time do you have? If you’re looking for a quick list of rules for bidding on a government job, I’ve got good news and bad news. Let’s start with the good: if you’re a small business, the…

You’ve got to spend money to make money — and the U.S. government does both. Literally. As the world’s largest purchaser, the government spends billions every year. However, the only thing it makes is money. That means the government relies on private businesses, large and small, for almost everything else. Curious…

It should come as no surprise that the U.S. Government is our nation’s biggest purchaser of goods and services. What is impressive is that 23 percent of that spending, amounting to $115 billion, is set aside specifically for small businesses. So, what does it take to bid on government contracts…

$100 billion is on the table. Will you take it? According to the U.S. Small Business Administration (SBA), the government awards nearly $100 billion in contracts to small businesses every year. However, all government contracts are not created equal. Some contracts may not pay enough to be worth your while,…

Make more money. Be your own boss. Spend less time on the road, and more time with your family. There are many reasons why you may want to start your own freight brokerage, and the payoff can be huge. However, according to Bloomberg, 8 out of…

The October 1 deadline for renewing your annual freight broker’s bond and license is fast approaching. Unfortunately, despite the shock and industry opposition following the increase from $10,000 to $75,000 in 2013, there is no point to putting off this expenditure in hopes that it will drop significantly. Instead, here…

The loads you broker to carriers may travel for days over the road, but the impressions conveyed by your brokerage via digital channels can be more immediate and impactful. That’s why it pays to invest in engaging with your customers online. Tap the power of web-based, social and mobile marketing…

It’s every freight broker’s worst nightmare: You finally landed the big account you wanted, and you’ve been awarded a contract to serve as freight broker. If you can keep your client happy, you could see your business grow by double. But on the day their first load arrives, you get…

When did signatures become so important? If you were back in the year 1473 (Islamic calendar 877-878, Hebrew calendar 5233-5234), you would find it hard to find a writing implement to use, and it would probably be even harder to find actual paper on which to sign. We take these…

For today’s generation, trucking doesn’t seem to hold much appeal. Long hours on the road, time spent away from family, and mediocre pay is leading to increasingly high turnover rates and driver shortages. In fact, according to the American Trucking Association, the industry needs 30,000 more drivers to meet current…

You’re a small business owner and you need financing. The first stop is your local bank where you get the sympathetic shake of the head from the loan officer. “Sorry, we can’t help with a loan but how about a checking account?” A checking account isn’t going to cut it…

When most people go to buy trucking insurance, they expect the obvious questions: How many trucks do you own? Where is your company domiciled? What commodities do you haul? What is your travel radius? Insurance companies use this information to formulate your premium. But, what else goes into rating a…

As the economy grows, one industry is standing out as the fastest growing small business industry—trucking. According to a recent article from Triumph Bancorp, parent company to Triumph Business Capital, the trucking industry has seen a 25 percent uptick in sales over the last year, indicating large growth. The American…

If you’re having trouble getting approved for a loan, you’re not alone. According to the 2014 Small Business Survey, 44 percent of firms who applied for loans failed to receive any credit. The biggest reasons? Low credit scores, insufficient collateral, and/or weak business performance. In recent years, it’s become…

Which do you need in your corner? Back in high school and all of my college years, I was an amateur boxer with a real passion for the sport. Boxers function on muscle memory, which is why professionals like Manny Pacquiao are able to throw over a thousand punches in…

Spend less time stressing about making payroll, and more time working on your business. In February of 2012, when I was eight months pregnant, my husband’s employer filed for Chapter 11 Bankruptcy. We lost our health insurance (even though we had been paying the premiums), and my husband’s bonuses and…

My first cousin, James is a long-haul trucker based out of Pennsylvania, and every time he comes through my hometown of Dallas, I meet him at a Denny’s and offer to buy him breakfast. He never says no. It’s not just because James likes his grits (and he does like…

When I tell people that I’m self-employed and I work from home, I know what they’re thinking. “Work from home? Yeah, right. She probably spends her day scanning Facebook, taking naps and doing laundry.” That is so ridiculous. I don’t do laundry. Kidding — but it is frustrating when people…

“Sir,” I said, “I drive a paid-off Honda Accord. I pay all my bills on time. And my house will be paid off in three months. How could I be more credit-worthy?” At 34 years old, I applied for a loan to purchase an investment property with 25% down, for…

The best factoring companies have your best interests in mind. Here’s how to select the right one for your business. I was perfectly happy with my streaming Internet service until a few months ago, when a lady on the phone called and convinced me to sign a two-year contract inviting…

Even if you already have your small trucking company up and rolling (pun intended), it's not too late to further refine your business. One refinement you might consider is choosing a niche. You'll often see that recommended in business articles for any industry, but it seems particularly necessary in trucking.

Recently I saw an idiom that said “Hustle until you no longer need to introduce yourself.” This got me to thinking on a couple of related thoughts. Why would you stop hustling when everyone knows who you are? Under what circumstances would it be no longer necessary to introduce yourself…

Nearly every small and micro-trucking company owner has asked this question several times. The smaller your operation, the more difficult it is to find the answer. So, many of us relegate ourselves to hauling wholesale (broker and load board) freight and leave the direct shipper freight to the bigger carriers.

The most common question I’m asked by owners/managers of small motor carriers is: “How do I grow my trucking company?” Moving your business to the next level isn’t based on luck. Growing a trucking company requires dedication and leaps of faith, but most of all it requires a solid business…

Maybe that hour ‘saved’ isn’t worth it There’s a joke going around the internet as a quote attributed to an old Indian chief concerning his opinion of Daylight Saving time. It says, “Only the government would come up with a plan where it is believed that if you cut of…

Call out the troops – again Here we go again; the idea that creating more government regulation is the solution to the woes of the trucking industry. There’s currently a piece of legislation in front of Congress, H. R. 7, American Energy and Infrastructure Jobs Act of 2012. This Act…

At the end of this month, the FMCSA will require all states to include truck drivers’ medical certification status and information on each trucker’s medical examiner’s certificate in each driver’s Commercial Driver’s License Information System record. There’s also the requirement to self-certify whether he or she is an interstate or…

I was recently tapped in an on-line conversation concerning the relevance of the fuel surcharge as a means of covering fuel costs. One poster stated: “Not to side with Timothy Brady, but the fuel surcharge is largely irrelevant. I could be saying that because I get one. What the FS…

Setting up a profitable freight lane takes more than just being in the right place at the right time. It’s more about understanding the dynamics of what freight is moving in what direction during certain periods of a month. A freight ‘lane’ can be any of a number of shapes…

A trucking company’s Break-even Points are the basis from which its hauling rate range is calculated. If the company owner or manager doesn’t know what it costs to operate a business, then success is very elusive. Many small trucking businesspeople are unsuccessful because they fail to cover the company’s cost…

Technology can be used either way By Timothy D. Brady EOBR technology is awesome, as a potential tool. But like any tool, it’s how it benefits everyone who uses it. But I have the same apprehension and fear as when I tested the QUALCOMM system back in its beginnings in…

(Even “cheap freight” pays something) By Timothy D. Brady The pitfalls of driving a trucking route without paying freight should be avoided. Some points I find it interesting: first, that there are still truckers who think if they can make a static rate per mile they’ll earn enough to…

Trucking’s Shame “Keep it between the ditches” is highway slang for “drive safe.” This series is provided as a public service by Advance Business Capital. From Time Magazine: “Adriesue (“Bitsy”) Gomez, 33, is a “gear-jamming gal with white-line fever.” A woman truck driver from Los Angeles, she is also a…

Publish your Rules Circular and prosper By Timothy Brady Last week Rep. Peter DeFazio, D-Ore, introduced a bill requiring the DOT to study industry detention practices and establish a maximum number of hours that drivers may be detained without being paid. The Government Accountability Office recently surveyed 300 truckers. 68%…

By guess and by golly won’t work By Timothy Brady According to Logistics Management 2011 Rate Outlook (https://logisticsmgmt.com/article/2011_logistics_rate_outlook/)“Volatile oil and diesel prices, capacity shortages, another looming driver crisis, debilitating regulatory uncertainties, and an improving economy have led industry analysts across all modes to one conclusion: Shippers will have to…

A deeper discount? Better hold onto your shirt By Timothy Brady Under the current economic atmosphere, large segments of the trucking industry have fallen into the trap of “Volume Discounting.” The greater volume a customer has to ship, the lower his shipping cost. While this works to a point, beyond…

You do what you gotta do By Timothy Brady Have you ever been rolling down the interstate, suddenly looked at the fuel gauge and realized: “I’m not sure I’ll make it to where I was going to fuel next.” All kinds of thoughts start going through your mind. Where’s the…

Niche Hauling: a geographic area, commodity, particular service, unique method, or specialized market for which a small trucking company is best suited. For the small or start-up trucking company, the highway to success is to find a specific niche which is not filled by the more traditional, larger trucking companies.

How important is knowing your Break-Even Point when you are a trucker? I’m constantly saying, “You’ve got to know your Break-Even Point!” But is it that important? According to Renee Cloud, of Clerical Business Solutions, a business management company providing business consulting & administrative support (virtual assistant services): “A number…

In the last blog, we went through the process of determining the value of a load, but that was only the first step in selecting which loads to haul and which ones to leave on the dock. Now for the next step, looking at the quality of a load. Value…

How to make a profit in today’s trucking industry. Are you asking yourself if you can really make a profit in trucking today, especially with fuel going up again and the freight still not recovering? That’s the 64,000-dollar question for most trucking companies. I’d still say, yes, you can make…

What is lane density? This is a term you may or may not have heard in the course of doing business as a trucker. But as you’re about to see, it’s very important in determining whether you are profitable or not. This applies to a single truck operation or multiple…